What are the Key Tax Changes in 2020 and What You Need to Do...

2020 Changes / Key Announcements

Below is a summary of the changes to be aware of and announcements that will potentially affect you for the year ending 30th June 2020, or will come into effect as of 1st July 2020.

1. Personal Income Tax Rates

2019/2020 Financial Year

Taxable Income Tax Rate %

$0 - $18,200 0%

$18,201 - $37,000 19%

$37,001 - $90,000 32.5%

$87,001 – $180,000 37%

$180,001 plus 45%

(plus 2% Medicare levy where applicable)

2020/2021 Financial Year

Taxable Income Tax Rate %

$0 - $18,200 0%

$18,201 - $37,000 19%

$37,001 - $90,000 32.5%

$90,001 – $180,000 37%

$180,001 plus 45%

(plus 2% Medicare levy where applicable)

*It is proposed from 1st July 2022 that there will be an increase in the tax thresholds to reduce the tax paid by taxpayers.

Note: The low income offset is $445. This offset will reduce by 1.5 cents for every $1 of taxable income over $37,000. It phases out when the taxable income is $66,667

2. Medicare Levy – Low Income Threshold

For the 2019/2020 income year, Medicare Levy will be incurred when the incomes are above:

- Individuals $27,997

- Families $47,242

Plus $4,339 for each dependent child.

The Medicare levy will now stay the same at 2.0% from 1st July 2020.

3. Motor Vehicle – Statutory Formula

a. FBT for Business

The Statutory Formula method to calculate the taxable value of the private use (Fringe Benefit) of a vehicle is a flat 20% statutory rate of the cost of the car. It is no longer based on kms travelled per year.

Important Note: Keeping a valid 3 month logbook is extremely important to be able to claim the actual cost method!

b. Cents per KM for Individuals

The Motor Vehicle Statutory Formula claim for the cents per kilometre for individuals is 68 cents per kilometre for 30th June 2020. There is only one single rate for all engine sizes. Individuals will only be able to claim cents per kilometre method or logbook method. You can no longer claim 12% of original value method or one third of actual expenses method. It is proposed that the rate will increase to 72 cents per km from 1st July 2020.

4. Superannuation Contributions (concessional)

The maximum amount that taxpayers can contribute into superannuation as concessional contributions are:

Year ending 30th June 2020 is $25,000

Year ending 30th June 2021 is $25,000

Important Notes:

- All individuals under the age of 75 can claim an income tax deduction for personal superannuation contributions. There will be no more 10% test to claim a tax deduction for personal contributions. Therefore, partially self-employed and partially employed (wages) and individuals whose employers do not offer salary sacrifice arrangements will benefit from proposed changes. Once you reach 65 years of age, you must satisfy the work test.

- Individuals with a superannuation balance of less than $500,000 can make additional concessional contributions if they have not used all their cap in the previous 5 years, on a rolling basis on unused amounts accrued from 2018/2019 financial year. So the 30th June 2020 is the 1st year you can use any unused balance from2018/2019.

- From 1st July 2019, an exemption from the work test for voluntary contributions to superannuation for people aged 65-74 with superannuation balances below $300,000 will be introduced.

- The superannuation co-contribution is when the government contributes upto $500 into your superfund when you make a $1000 personal contribution into your superfund. You must be under 71 years old, have less than $1.6 million in your superfund and 10% of your income must be from employment or carrying on a business. The income threshold is $38,564 for 30th June 2020 to get the maximum of $500. It then phases out until your income reaches $53,564.

5. Superannuation Contributions (non-concessional)

The non-concessional contribution cap (contributions for which you do not claim an income tax deduction) is:

2019 – 2020 Income Year $100,000

2020 - 2021 Income Year $100,000

People aged under 65 years may be able to make lump sum non-concessional contributions of up to three times their non-concessional cap over a 3 year period (lump sum $300,000)

Important Notes:

- Non-concessional contributions can only be made if your total superannuation balance is under 1.6million.

- From 1st July 2017, the government has removed the tax exemption on earnings of assets supporting Transition to Retirement income streams, being income streams of individuals over preservation age but not retired. The earnings will be taxed at 15% and the change is proposed to apply irrespective of when the Transition to Retirement commenced.

- From 1st July 2017, the government has introduced a $1.6million superannuation transfer balance cap on the total amount of accumulated superannuation an individual can transfer into pension phase. Under the proposed changes:

- Subsequent earnings on this pension balance will not be restricted

- If an individual accumulates amounts in excess of $1.6million they will be able to maintain this excess amount in accumulation phase account (where earnings will be taxed at the concessional rate of 15%)

- The low income spouse superannuation tax offset income threshold for low income spouses is $37,000. The offset will phase out when income reaches $40,000. The low income spouse offset provides up to $540 per annum when $3,000 is contributed into your spouse’s superfund.

- People aged 65 or over can make non-concessional contributions into superannuation of up to $300,000 from proceeds of selling their home. These non-concessional contributions will be in addition to the caps, age tests and the $1.6million balance test.

6. Home Office Deduction

The two methods for claiming a home office deduction for employees on their tax return are:

- Fixed Rate per hour method (for 30th June 2020 this is 52 cents per hour if you keep a four week diary)

- Actual Method (based on the proportion of additional expenses as a result from working from home)

Important: Due to Covid-19, the ATO will allow you to claim 80 cents per hour for working from home from 1st March 2020 to 30th June 2020. This however covers all expenses for working from home.

7. Minors (Children under 18 years)

Families distributing money to children from Family Trust’s will need to be aware that they can only distribute $416 tax free for 30th June 2020 year.

8. Additional Tax on Superannuation Contributions – High Income Earners

In the 30th June 2020 year, Individuals with income greater than $250,000 will have their super contributions taxed at 30% and not 15% (this has been in place since 1st July 2012).

Note:

- Income is taxable income plus reportable fringe benefits, reportable superannuation contributions and any total net investment loss

- Super contributions include super guarantee and salary sacrifice

- The tax is payable by the individual client not the superfund however you can apply to have the money released from your superfund.

9. Superannuation Guarantee

The SG rate will stay at to 9.5 per cent. This will remain until 2021/2022 and then increases will be by 0.5 per cent each financial year until 12 per cent is reached. The proposed future increases each year are:

Financial Year Minimum Superannuation Guarantee Rate

2019/20 9.50%

2020/21 9.50%

2021/22 10.00%

2022/23 10.50%

2023/24 11.00%

2024/25 11.50%

2025/26 12.00%

For individuals to claim a deduction for personal contributions, you must have a valid written notice (deduction notice) advising you intend to claim a tax deduction and a written acknowledgement from the superfund.

10. Changes To Family Trusts And Income Resolutions

Trustees must ensure that trust income is distributed by an income distribution resolution/minute by the 30th June 2020. These resolutions must show what trust income each beneficiary is entitled to, and the streaming of franked dividends and capital gains if applicable.

Trusts with older deeds should have these reviewed to ensure the definition of income complies with current legal definitions in the tax act and that the deed allows for streaming of capital gains and franked dividends. The trust deed must also state all required beneficiaries.

11. Changes to Rental Properties

a. Since 1st July 2017, travel expenses will be disallowed for inspecting, maintaining or collecting rent for residential rental properties.

b. Since 9th May 2017, investors who purchase residential investment properties will only be able to claim depreciation on plant and equipment on new acquisitions of plant and equipment

- Investors who purchase new plant and equipment can still claim depreciation after 9th May 2017

- From 9th May 2017, investors cannot claim depreciation on any plant and equipment that was purchased with the property or was used previously for private use

- Existing property investors, before 9th May 2017, can continue to claim depreciation

- All investors can continue to claim the depreciation on the building costs from 9th May 2017

c. From 1st July 2019, the government will deny deductions for expenses associated with holding vacant residential or commercial land, including interest on finance for the acquisition of the land. Deductions for expenses associated with holding land will be available once a property has been constructed, it has received approval to be occupied and is available for rent. Denied deductions will not be able to be carried forward for use in later income, however, denied deductions can be included in the cost base of the land.

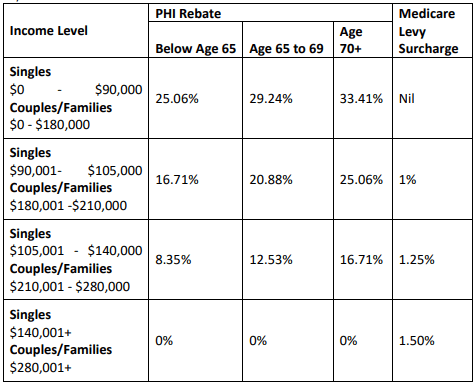

12. Changes To Private Health Insurance Rebate And Medicare Levy Surcharge

The private health insurance rebate is now income tested and the Medicare levy surcharge will be increased based on your income if there is no appropriate private hospital cover for the year. The following table summarises the changes to the private health insurance (PHI) rebate and the Medicare levy surcharge (if you do NOT have the required hospital cover)based on the income levels from the 1st April 2020 (the rebate % has decreased from last year):

(For families with more than one dependent child, the relevant threshold is increased by $1,500 for each child after the first)

13. Change To Depreciation for Small Businesses

Small businesses with aggregate annual turnover of less than $50 million can immediately deduct assets they start to use or install ready for use, provided the asset costs less than $30,000 (GST excl). This will apply for assets acquired and installed ready for use at 30 June 2020.

From the 12th March 2020 the instant asset write-off threshold has been increased to $150,000 (from $30,000) It is proposed that this concession is to extend until 31st December 2020.

Note: this is for small business entities, not employees or rental properties

14. Higher Education Loan Programme (“HELP”) & Trade Support Loan (TSL) – repayment thresholds

For 2019/2020 the threshold and repayment rate to pay back debt is:

Repayment Income Repayment Rate

Below $45,881 Nil

$45,881 – $52,973 1.00%

$52,974 - $56,151 2.00%

$56,152 - $59,521 2.50%

$59,522 - $63,092 3.00%

$63,093 - $66,877 3.50%

$66,878 - $70,890 4.00%

$70,891 - $75,144 4.50%

$75,145 - $79,652 5.00%

$79,653 - $84,432 5.50%

$84,433 - $89,498 6.00%

$89,499 - $94,868 6.50%

$94,869 - $100,560 7.00%

$100,561 - $106,593 7.50%

$106,594 - $112,989 8.00%

$112,990 - $119,769 8.50%

$119,770- $126,955 9.00%

$126,956 - $134,572 9.50%

$134,573 and above 10.00%

Australians who have a HELP or TSL and are residing overseas, will be required from 1st July 2017 to make repayments against their debt based on their 2019/2020 worldwide income. Overseas debtors are required to update their contact details via MyGov within 7 days of leaving Australia.

15. Small Business Income Tax Offset (SBITO)

Individuals will receive a 8% tax discount as a non-refundable tax offset on business income. This includes Sole Traders, Partners in Partnership and Trust Distributions where the entity carries on a business. The entity must be a small business entity with a turnover of under $5million. The tax discount will be capped at $1,000 per individual for each income year.

From 2020/2021 the tax offset increases to 13% and 16% in 2021/2022. However the cap is still $1000.

16. Reducing the Company Tax Rate

For the 30th June 2020 financial year, the company tax rate is 30%. However companies that are a “base rate entity” must apply the 27.5% company tax rate.

A base rate entity is a company that both:

- Has an aggregated turnover of less than $25 million

- Has 80% or less of their assessable income as passive income (passive income is distributions, rent, interest income, gains on securities, capital gains, and an amount from a partnership or trust to the extent it is traceable to an amount that is passive income)

Note: the current maximum franking credit rate for distribution will be 27.5% for these Base Rate Companies in 2019/2020.

For 2020/2021 the company tax rate for base rate entities will be 26% and then 25% for 2021/2022 and later income years.

17. Zone Offset Change

Since 1st July 2015, all FIFO (Fly In, Fly Out) and DIDO (Drive In, Drive Out) workers will not be able to claim the zone rebate for the zone they work in. The zone rebate entitlement will only relate to the zone of their normal place of residence. Taxpayers who actually reside in a zone can continue to claim the zone rebate.

18. Single Touch Payroll

All Employers from 1st July 2019 must be setup for Single Touch Payroll (STP). With STP you report all employee’s payroll information such as wages, PAYG withholding and superannuation to the Tax Office each time you pay staff through your software.

A concession starting date of 1st July 2021 has been given to closely held employees in businesses were the closely held employees are family members.

19. Low and Middle Income Tax Offset

If your income is less than $126,000, you will get some of the low and middle income offset. The maximum offset is $1,080. The rebate is based on your taxable income.

If your taxable income:

- Does not exceed $37,000 the offset is $255

- Exceeds $37,000 but is no more than $48,000, you will be entitled to $255 plus 7.5% of the excess above $37,000 to a maximum of $1,080

- Exceeds $48,000 but is no more than $90,000 you will get the maximum offset of $1,080

- Exceeds $90,000 but is no more than $126,000 you will be entitled to $1,080 less 3% for each $1 above $90,000. Therefore is phases out to $0 offset when your income is $126,000 or more

20. Reducing Claim Period for Family Assistance Lump Sum Claims

Families that choose to wait until the end of the financial year to claim their FTB entitlement or child care benefit will have a grace period of one year. Therefore, all 2019 tax returns must be lodged by 30th June 2020 and all 2020 tax returns must be lodged by 30th June 2021.

21. New COVID 19 measure to help business and individuals

As part of the federal and state government response to COVID 19 the following help is available:

- New home office set rate per hour for employees work deduction from 1st March 2020 of 80 cents per hour

- JobKeeper payments for eligible businesses where their business turnover has decreased by 30% for the test period for the period 1st April 2020 to 27th September 2020. The amount is $1,500 per fortnight for eligible employees.

Important: Remember you must complete and lodge the monthly jobkeeper declaration within 7 days at the end of each month.

- Cashflow Boost: Employers will receive a tax free cashflow boost payment comprised of two parts:

1. First Cashflow Boost payment is based on your PAYGW on March 2020 BAS for Quarterly lodges and the March 2020 BAS and April and May 2020 IAS’s for monthly lodgers. It is a minimum of $10,000 and a maximum of $50,000

2. The second boost payments for eligible employers are equal to the amount received in the first cashflow boost. Again a minimum of $10,000 and max of $50,000. It will be paid in two instalments for quarterly lodgers on the March and September 2020 BAS lodgements. For monthly lodgers it will be paid in 4 instalments on the March 2020 BAS, the July and August IAS and finally on the September 2020 BAS

- Early access to superannuation for the unemployed, or since 1st January 2020 their work hours have been reduced by 20% or more, or sole traders where their turnover has been decreased by 20% or more. If you are eligible you can access $10,000 upto 30th June 2020 and $10,000 from 1st July to 24th September 2020.

- The minimum pension payment for pension payments to members can be reduced by 50% for the 30th June 2020 and 30th June 2021 financial years. The minimum pension rate is based on your age so you need to check what your minimum rate is.

- Increase in the immediate write-off threshold to $150,000 GST exclusive of a depreciating asset for small businesses from 12th March 2020

- ATO lodgement and payment deferrals for 2019 tax returns

- Ability to vary PAYGI down to $0

- WA Payroll tax will be waived for businesses from March to June 2020

- Small Businesses will receive a once-off $2500 credit on their current and future electricity bills

- Wage subsidy of 50% of an apprentice or trainees wage

- $10,000 business grant for eligible small businesses

- Centrelink will pay an extra $550 per fortnight supplement to new and existing jobseeker, youth allowance and parenting payments. There will be no asset in determining entitlements for 6 months and the spouse income test has been increased from $48,000 to $79,762 before the entitlement reduces to Nil

Reminder of Things to Consider Before 30th June

- Consider making the $1,000 personal contribution to qualify for the super co-contribution before the 30th June if your taxable income will be below the thresholds.

- Consider making a spouse contribution into superannuation if you qualify for the rebate.

- Ensure your 3 month logbooks have been kept on vehicles.

- Make sure you have receipts for your tax deductions.

- Review the need to sell capital assets to obtain any capital losses if you have made any capital gains during the year.

- Obtain/prepare a summary of child support paid during the year if you are paying child support or child support you may have received, if you are receiving.

- Businesses:

- Make sure you have odometer readings for all work vehicles.

- Super must be paid for staff by the 28th However to get the deduction in the 2019/2020 year it must be paid to the super clearing house before the 21st June (or received by Superfund if paid by transfer).

- After the final pay has been processed using the Single Touch Payroll you need to do final reconciliation

- Trust Resolutions/Minutes for all trusts must be prepared and signed before 30th June 2020.

- Businesses in the various required industries must lodge their payment annual reports for payments made to contractors during the year by 28th August 2020.

- Individuals:

- Home office claim – ensure you have a 4 week diary recording hours worked from home for work. Must be kept to claim home office deduction.

- Internet claim – ensure you have kept a 4 week diary recording internet usage (hours used for work/hours used personally) to support your work internet claim. This must be kept to claim home internet as a work deduction.

- Motor Vehicle deduction – ensure you keep a 4 week diary of vehicle kilometres used for work to support the tax deduction.

Need help with your accounting?